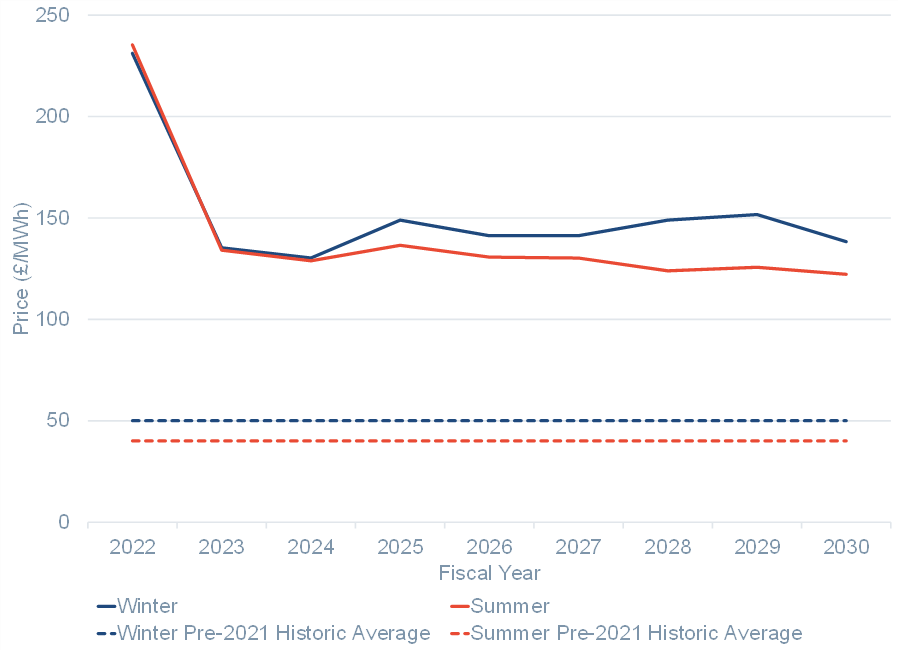

Research from Cornwall Insight looking at Great Britain’s (GB) Power Market out to 2030 has shown energy prices will remain in excess of £100/MWh annually. This is significantly above the five year pre-2021 historic average of £50/MWh in Winter and the even lower prices in pre-2021 Summer.

Cornwall Insight’s Benchmark Power Curve (BPC) for the British Electricity Market which covers England, Scotland, and Wales, shows that while prices will drop from the current levels, they will remain high. Prices are expected to rise to £150/MWh in Winter 2025 due to closures of nuclear power stations, delays to Hinkley C, and increasing high-cost peaking capacity.

Renewable generation capacity will rapidly increase to meet targets and will help meet rising demand; however, marginal gas-fired generation sets power prices.

Figure 1: Power price forecasts – average per fiscal year

Source Cornwall Insight Benchmark Power Curve

Tom Edwards, Senior Modeller at Cornwall Insight said:

“While we are used to seeing headlines depicting energy prices at an all-time high, unfortunately, while prices will reduce, our modelling shows that pre-2021 prices are not making a comeback this decade and likely beyond.

“Rising EU demand for non-Russian gas has pushed up gas prices across the world, and these higher prices have increased production costs for power, with gas set to remain the marginal fuel source for producing power throughout the remainder of the 2020s. With all GB coal capacity due to close by April 2024 and many nuclear power stations coming to the end of their lives, high power prices will continue to feed through into consumer bills.

“To stabilise and reduce power prices will take two important steps. Firstly, reducing our reliance on volatile fossil fuel prices by diversifying supplies and increasing renewables power generation. The government ambition to build new nuclear and reach 50GW of offshore wind by 2030 is an important and ambitious step but it should also be matched by removing barriers to onshore wind and solar PV.

“Secondly, we need to increase the flexibility and stability of the power supply. Ultimately, we must ensure we have the capacity to back-up short-term variations in renewables power supply, as well as the infrequent longer periods of low winds. This will involve, yet unpromised, investment in long duration energy storage including pumped storage and hydrogen storage.

“Our power curve does little to alleviate consumer or supplier concerns over energy prices, and the government and other policy makers are simply not providing protection for power prices in the shorter-term. The next decade and beyond will see significant changes to the energy generation technology mix with renewables becoming more and more important. We must make sure that not only do we plan for long-term generation, but we work to design a wholesale market which supports investment in new low carbon capacity at the lowest possible cost to consumers. We welcome BEIS announcement of the Review of the Energy Market Arrangements (REMA) as part of the energy security strategy.”

–Ends

Notes to Editors

For more information, please contact: Verity Sinclair at v.sinclair@cornwall-insight.com

To link to our website, please use: https://www.cornwall-insight.com/

About the Cornwall Insight Group

Cornwall Insight is the pre-eminent provider of research, analysis, consulting and training to businesses and stakeholders engaged in the Australian, Great British, and Irish energy markets. To support our customers, we leverage a powerful combination of analytical capability, a detailed appreciation of regulation codes and policy frameworks, and a practical understanding of how markets function.